Table of Contents

Limits on How You Spend a Viatical Settlement

If you’ve recently sold your life insurance policy through a viatical settlement, you might be wondering: “Are there any limits on how I can spend the money?”

The short answer is — no, there usually aren’t strict limits. Once the transaction is complete, the funds are yours to use as you wish. But before you start spending, it’s smart to understand the guidelines, implications, and potential consequences that come with a viatical settlement.

In this article, I’ll explain what a viatical settlement is, how the process works, and the realistic limitations — both legal and financial — on how you can use the money.

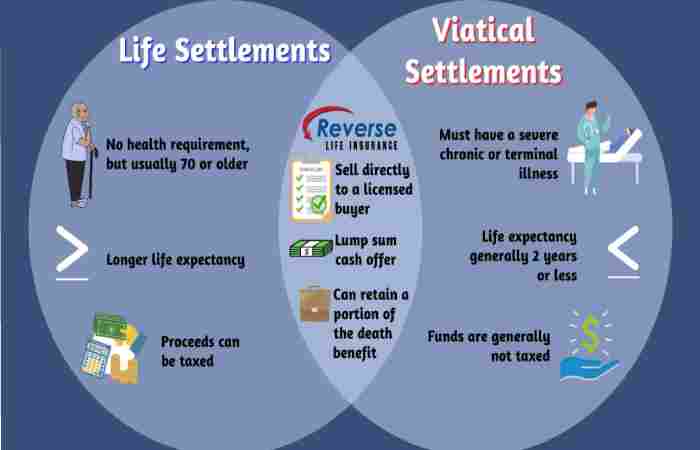

What Is a Viatical Settlement?

A viatical settlement allows someone who is terminally or chronically ill to sell their life insurance policy to a third party (called a viatical settlement provider). In return, the policyholder gets a lump-sum cash payment that’s usually less than the policy’s death benefit but more than its surrender value.

How It Works

-

You sell your policy to a licensed provider.

-

The provider becomes the new policy owner and pays the future premiums.

-

When you pass away, the provider collects the full death benefit.

This arrangement gives patients immediate access to funds when they need them most — often for medical expenses, caregiving, or simply improving quality of life.

Do You Have to Spend the Money a Certain Way?

Here’s the good news: There are no legal restrictions on how you spend your viatical settlement.

Once you receive the payment, it’s your money. You can use it for anything — from medical treatment to paying off debt, buying a car, or even taking that long-awaited vacation.

Common Ways People Use Viatical Funds

-

Medical costs: Covering treatment, medication, or specialized care.

-

Debt repayment: Paying off credit cards, mortgages, or loans.

-

Living expenses: Rent, utilities, groceries, or transportation.

-

Bucket list goals: Traveling, family experiences, or personal comfort.

-

Estate planning: Supporting loved ones or donating to charities.

That said, even though there are no spending limits, there are important considerations to keep in mind.

1. Tax Implications and Reporting

Even though you can spend the money freely, you should understand how it affects your tax situation.

Tax-Free in Most Cases

Under U.S. law (IRC §101(g)), if the policyholder is terminally ill — certified by a physician — the proceeds from a viatical settlement are generally tax-free.

However, if you’re considered chronically ill (not terminal), the tax exemption may only apply if the funds are used for qualified long-term care services or medical expenses.

Why It Matters

-

Spending the funds on non-medical purposes could trigger taxable income in some cases.

-

Always consult a tax advisor or CPA before making large purchases.

-

State tax laws may differ, so it’s smart to double-check.

In short: you have the freedom to spend your viatical settlement however you want — but tax consequences may depend on how you use it.

2. Effect on Government Benefits

If you receive Medicaid, Supplemental Security Income (SSI), or other needs-based benefits, the lump sum from a viatical settlement might affect your eligibility.

Here’s Why

-

These programs have income and asset limits.

-

A large payout could push you over those limits, causing benefits to be reduced or temporarily suspended.

What You Can Do

-

Work with a financial planner or benefits specialist before finalizing the settlement.

-

Consider placing funds in a Medicaid-compliant trust if you need to preserve benefits.

-

Keep documentation of all medical expenses paid with the settlement.

So, while there are no spending limits, how you manage and report that money can affect your long-term financial stability.

3. Potential Impact on Family and Estate Planning

Using your viatical settlement wisely can also support your loved ones — but you’ll want to plan it carefully.

Why Planning Matters

Once you sell your life insurance policy, your beneficiaries will no longer receive the death benefit. That means your family won’t get any payout from that policy when you pass away.

Smart Uses

-

Setting aside part of the settlement for family expenses or future care.

-

Creating or updating your will and estate documents.

-

Making gifts or donations while ensuring your own financial security.

Remember: your viatical settlement gives you freedom, but it also replaces the policy’s future value — so balance today’s comfort with tomorrow’s needs.

4. Emotional and Financial Discipline

It’s easy to feel a sense of relief — or even excitement — after receiving a large lump sum. But spending impulsively can lead to regret.

Tips for Responsible Spending

-

Make a plan: List priorities like medical bills, living expenses, and future security.

-

Avoid risky investments: High-return promises often come with high risk.

-

Work with professionals: A financial advisor can help you stretch your money.

-

Keep emergency funds: Set aside some cash for unexpected costs.

While there’s no legal limit, financial discipline ensures your viatical settlement truly serves its purpose — improving your quality of life and peace of mind.

5. Legal and Provider Guidelines

Even though you can spend your payout freely, some limitations may apply during the process, depending on the provider and your state.

Examples of Provider-Based Rules

-

You may need to disclose how you plan to use the funds as part of the application.

-

Certain states require counseling or financial advice before approving a settlement.

-

Providers must follow state insurance regulations, including transparency and disclosure laws.

These rules exist to protect you from predatory practices, not to control your spending after the payout. Once you receive your money, you’re in full control.

6. Why Responsible Use Matters

Freedom comes with responsibility. A viatical settlement is often a once-in-a-lifetime opportunity to ease financial burdens and create comfort during illness.

But misuse of the funds can cause long-term stress. Spending it all too fast may leave you short on cash for essential care later.

A Balanced Approach

-

Use a portion for immediate relief — like medical costs and debt payoff.

-

Save or invest part of it (safely) for ongoing needs.

-

Consider your family’s future needs and final expenses.

In other words: while there are no restrictions, the smartest approach is to spend intentionally and prioritize what matters most.

Key Takeaways: Are There Limits on a Viatical Settlement?

Let’s recap everything in plain language:

| Aspect | Are There Limits? | What to Keep in Mind |

|---|---|---|

| Spending | No legal limits | You can use the money however you wish. |

| Taxes | Sometimes | Terminally ill = usually tax-free; chronically ill = depends on use. |

| Government Benefits | Yes, possible impact | Lump-sum payments may affect Medicaid/SSI eligibility. |

| Family & Estate | Indirect impact | Beneficiaries won’t get policy payout after sale. |

| Provider Rules | Limited during process | Some states require disclosures or counseling. |

So, while there’s no law controlling your spending, understanding these areas ensures you avoid unwanted surprises.

Conclusion: Freedom with Responsibility

When it comes to limits on how you spend a viatical settlement, you have complete freedom — but also the responsibility to make thoughtful decisions.

The settlement gives you financial flexibility at a critical time. You can use it for:

-

Medical bills

-

Daily living costs

-

Debt relief

-

Family support

-

Or even fulfilling lifelong dreams

Just remember to consult a tax advisor, financial planner, or benefits counselor before making big moves. The choices you make today can determine your comfort, security, and peace of mind tomorrow.

Ultimately, the money is yours — and how you spend it should reflect your values, priorities, and goals for the time ahead.